The KelpDAO security breach, which resulted in the reported loss of roughly $290 million, has become more than a standalone exploit. The incident reveals how tightly coupled DeFi lending, restaking, and collateral loops have become, turning a single protocol failure into a market-wide liquidity event.

Cross-Market Liquidity Stress

Nearly a week ago, attackers suspected to be part of the North Korean Lazarus Group compromised the verification nodes of Kelp DAO’s cross-chain bridge, allowing them to bypass security checks and fraudulently withdraw $293 million in rsETH.

Sponsored

Following the exploit, the stolen assets were reportedly used as collateral to borrow around $200 million in ETH on lending platforms such as Aave. This created exposure to potentially impaired collateral within lending markets and contributed to heightened risk sensitivity across DeFi protocols, as users rushed to pull their money out before the system collapsed.

The exploit led to a broader sector-wide exodus, with double-digit percentage declines across multiple protocols.

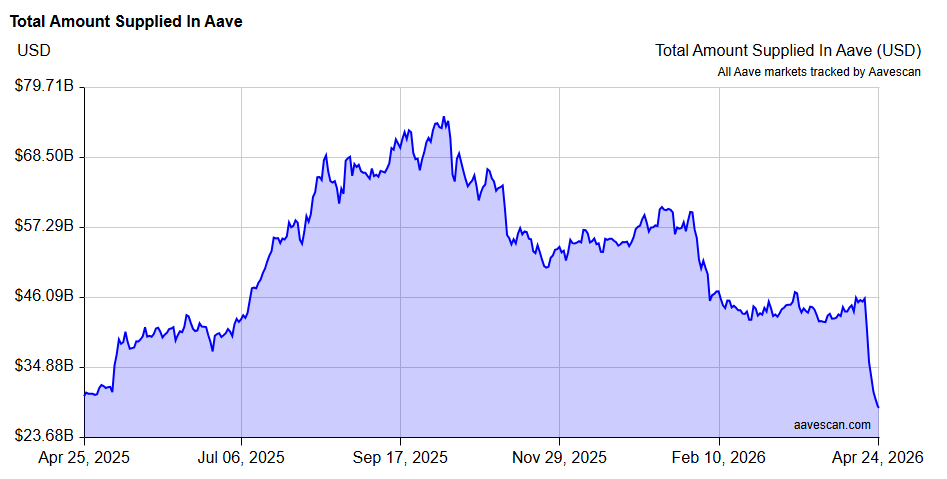

In the days following the incident, Aave alone recorded roughly $15 billion in outflows, with liquidity stress spreading across various other DeFi platforms.

Source:

Source:

Major platforms saw significant losses: Aave fell 32.5%, Spark dropped 31%, while Solv Protocol and EulerDAO declined by 68% and 52%, respectively.

Even established protocols like Curve and Pendle weren’t spared, recording declines of 11% and 12.5% as capital fled the ecosystem.

The result was a sharp shift in market conditions, available liquidity thinned, and borrowing conditions tightened.

A Coordinated Industry Response

In response to one of the year’s largest crypto security incidents, industry participants launched a coordinated effort to contain the fallout.

Aave led a coalition dubbed “DeFi United” aimed at absorbing up to $230 million in bad debt, with several major players stepping in to help stabilize the system.

Aave founder Stani Kulechov personally pledged 5,000 ETH, while Mantle proposed a 30,000 ETH credit facility to support the protocol. Other participants, including Lido (2,500 stETH), Ether.fi (5,000 ETH), and Golem (1,000 ETH), have also joined the effort, signaling a rare moment of industry-wide coordination to prevent broader disruption in lending markets.

Implications for DeFi Risk Models

The incident is expected to influence how risk is assessed across DeFi lending markets. In the short term, liquidity remains uneven, and borrowing costs have increased as users reduce exposure and unwind leveraged positions. Activity involving restaking-based collateral has declined.

Over the longer term, lending protocols are reviewing collateral frameworks and eligibility criteria. Some protocols are reassessing exposure to more complex or composable assets. Market pricing of risk has adjusted following the event, with more cautious lending conditions across parts of the ecosystem.

Why This Matters

The KelpDAO incident demonstrates that DeFi is no longer a set of isolated protocols, but a deeply interconnected financial system where failure in one layer can rapidly propagate across lending, restaking, and liquidity markets. It exposes structural weaknesses in how complex collateral assets such as liquid restaking tokens are evaluated and accepted.

The coordinated response from major actors also suggests that “decentralized” markets already rely on informal coordination layers during crises, effectively introducing de facto systemic risk management.

Discover DailyCoin’s hottest crypto news today:

Algorand Gets a Massive Glow-Up Via Coinbase Quantum Paper

XRP’s ‘Global Bridge’ Endgame: Washington Scrambles To Regulate?

People Also Ask:

Systemic risk in DeFi refers to the possibility that a failure in one protocol can spread across the broader ecosystem due to interconnected lending, collateral, and liquidity relationships.

Lending protocols are central liquidity hubs. If collateral loses value or becomes illiquid, these platforms can accumulate bad debt and transmit stress to other parts of the ecosystem.

It means that risks are not isolated to a single protocol. Users may be indirectly affected by failures elsewhere in the ecosystem, especially when using leveraged or collateralized positions.