Berky’s Perspective on the Era of Agents: Letter to Investors for Berky Investment’s Flagship Product 2026

Since the end of 2022, after the sensational emergence of ChatGPT, the wave of artificial intelligence has surged repeatedly. Investor enthusiasm for artificial intelligence investments remains high. Recently, Anthropic, OpenAI, and X.AI under SpaceX all have IPO plans, which has once again pushed the market’s attention to artificial intelligence to its peak.

Coincidentally, these three companies above represent the most important unlisted holdings in Baillie Gifford’s flagship product, the Scottish Mortgage Investment Trust (SMT). Their eventual listing will bring considerable returns to SMT.

On the flip side, there is ongoing debate in the market about artificial intelligence: the immense impact on the software industry, the sustainability of huge capital expenditures, US-China AI competition, which industries could be replaced, and so on.

Artificial intelligence is arguably Baillie Gifford’s core area of interest. One of Baillie’s fund managers once said, “About 95% of the portfolio holdings will in various ways directly engage with AI.”

However, do not assume Baillie Gifford only focuses on pure artificial intelligence concepts—they concentrate on practical applications. “This is not an ‘AI portfolio’, but rather an investment portfolio made up of businesses that use AI as a universal tool.” Some of Baillie’s analysts have even said: “In the future, we will no longer specifically talk about AI; it will be completely integrated into our lives and will ultimately manifest as increases in revenue and productivity.”

From this perspective, we can see that Baillie Gifford does not treat AI as an independent “investment theme”; instead, they view it as a universal tool, like the Internet, that will permeate all industries.

Even more interesting is that throughout Baillie Gifford’s hundred-year history, they have witnessed a vast number of technological transformations, experiencing development opportunities and the bursting of bubbles during several rounds of revolution. From this standpoint, Baillie Gifford’s perspective on artificial intelligence is a fascinating topic.

Baillie Gifford’s flagship product, the Scottish Mortgage Investment Trust (SMT), has released its annual report. We previously shared the first part with fund manager Tom Slater. Now, we continue with the message from another SMT fund manager, Lawrence Burns, to investors, in which he focuses on artificial intelligence development and investment from Baillie’s perspective.

From Baillie’s viewpoint, AI has moved from the era of dialogue, through the era of reasoning, and is now entering the era of agents. Currently, the software industry is being greatly impacted, with AI rapidly replacing human coding. However, there are both losers and winners in the industry. The infrastructure of software will see greater development in the future. Moreover, agents in fields of knowledge—including law, finance, and consumer—will also have major impacts. The key is whether a business can maintain a durable competitive edge in the AI wave.

In addition, artificial intelligence is not limited to Silicon Valley; China also holds several advantages in the AI revolution, including: physical AI, high cost-performance, and productization capabilities. These advantages are driving the emergence of valuable enterprises in China amid this transformation wave.

Lastly, Baillie draws inspiration from the patterns found in past revolutions and how investors can respond accordingly.

Below is the letter to investors from Baillie Gifford’s Lawrence Burns 2026.

The Era of Agents

In January 2025, artificial intelligence company Anthropic posted annualized revenue of $1 billion. Fifteen months later, that number had already surpassed $3 billion. As far as records show, no company has achieved such organic revenue growth at this scale and speed. Anthropic is one of the Scottish Mortgage Investment Trust’s (SMT) private equity holdings and has helped pioneer the third era of generative artificial intelligence.

The first era was the dialogue era, which began at the end of 2022 with the release of ChatGPT by OpenAI, when models became able to reliably follow natural language instructions and handle two-way exchanges with users.

The second was the era of reasoning, starting in September 2024 with OpenAI’s o1 model. The model at that time learned to pause, think step by step, and

By late November 2025, with the launch of Anthropic’s Claude Opus 4.5, the arrival of the Agent Era became indisputable. Models can be assigned a goal and persistently pursue it across many steps: planning, using tools, reviewing their own work, and providing useful output without constant human prompting.

Each era builds upon the last, not replaces it. Today’s agents are reasoning models that have learned how to act, just as reasoning models were dialogue models that learned how to think.

The rise of agents has influenced our portfolio, impacting the structure of the software industry, the value of consumer companies, the rise of a parallel Chinese AI ecosystem, and the need to build physical supply chains capable of meeting insatiable compute demand.

Software

The influence of agents first manifests at scale in software. In the traditional software industry, work is digitized, highly valuable, with clear goals and rapid feedback.

Agents adapt quickly. Google’s CEO stated that 75% of new code is now written by artificial intelligence. The founder of one of our portfolio companies recently told us that its expenditure on AI coding tools for engineers now surpasses the payroll for human engineers. Furthermore, the return on investment from intelligent agent tools has been greater than from the engineers themselves. At Anthropic, artificial intelligence now writes 70% to 90% of the code.

We are moving toward a future where an ever-increasing proportion of software is built, operated, and used by agents. This has profound implications.

Firstly, it weakens the relationship between software value and number of “users” (licensed internal users), a metric that much of the industry’s pricing relies on. Secondly, it lowers the barrier to creating software, intensifies competition, and erodes the moat built on coding accumulation and complexity. Thirdly, it raises a deeper question: Where will each company’s value accrue—in the software application itself, or in the intelligent layer that understands tasks, leverages relevant data, and directs the work?

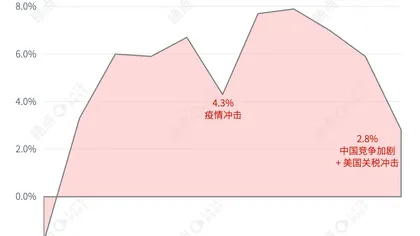

The market responded rapidly. In the past 12 months, the global software industry’s market cap has dropped by about $2 trillion. Some software re-pricing is perhaps justified: some companies’ previous valuations did not account for the impact of agents on pricing power, competition, and value capture.

However, the market’s re-pricing of the software sector has been indiscriminate, affecting all companies. Not all software companies are equal. Notably, there is a distinction between software serving human users and software providing foundational infrastructure relied on by other digital activities. If agents change how people interact with applications, the former may be at greater risk. The latter is more likely to benefit in the future, as agents drive greater downstream demand: data queries, security checks, compute workloads, payments, and identity.

Our software holdings lean more toward the infrastructure layer. If agents are to play a role within enterprises, then Rancher and Snowflake would organize the managed corporate data necessary for agents. Cloudflare provides the network and security layers on which agent applications can run, while also helping websites identify, control, and charge AI agents for access. Adyen and Stripe offer payment and trust infrastructure, enabling agents to transact securely on behalf of customers and merchants. The founders of Stripe have been careful not to exaggerate the pace of change; they believe agent businesses may emerge step by step, rather than in a sudden leap—but each incremental step in intelligence still requires programmable, authorized, and trusted financial rails.

Beyond Software

The impact of agents goes beyond software development. Most knowledge work, when broken down, can be summarized as: reading, writing, reasoning, and using software. These combined tasks can complete work. And these are precisely the capabilities agents now excel at. For a long time, tasks like drafting legal memos, synthesizing clinical trials, building financial models, or reviewing patent applications appeared highly specialized at the expert level but are cognitively generic in practice. The result: agents are not tools for just one industry but for many.

The same logic applies to consumer companies. Agents could become our shopping, financial, and daily assistants. If a horizontal AI assistant sits between the customer and the platform, it poses risks. However, the most powerful platforms control the assets necessary for agent work: trust, customer history, payments, credit, logistics, product catalogs, and merchant networks. Amazon, MercadoLibre, and Sea Limited are looking to build their own vertical agents to serve their platforms and facilitate shopping outside their platforms.

Nubank provides a comparable case in finance. Even before agents became popular, founder David Vélez told us that Nubank’s ambition was to be the private banker in every customer’s pocket. Agents make this more attainable: helping users manage bills, understand spending, choose when to borrow, build savings, and find the lowest rates in the market. Agents improve price transparency, tailor options to personal circumstances, and reduce friction in taking action. For Vélez, this is an opportunity; as a low-cost operator, Nubank is fully equipped to capture it.

Few companies will remain unaffected by the rise of agents. For some, agents will create new demand; for others, they will threaten current profit pools; and for many, the effect will be both. This will present a key challenge to our growth investing in the years ahead. SMT is well positioned to tackle it, as we invest in both public and private markets. Many of the companies shaping the AI frontier remain private, and our access allows us to better understand the pace of technology improvement, adoption, and the value that could ultimately be created.

Beyond Silicon Valley

Addressing this challenge also requires a geographical lens. It is easy to oversimplify artificial intelligence as a Silicon Valley story. For the vanguard of model capabilities, this is broadly accurate. But it is not complete. China is not just an AI follower; it is developing different strengths under different conditions.

The first is physical AI. Simulation is vital, but embodied intelligence progresses fastest when virtual training is combined with real-world deployment. China’s manufacturing base is important because it provides the world’s largest rollout capability for embodied intelligence. The highest volume of industrial robot installations, dense local supply chains, and supportive policies. The electric vehicle industry, which has already fused software, hardware, and cost-focused manufacturing, is the best evidence. One of our holdings, Horizon Robotics, sits directly at the intersection of AI and the real world and also aspires to expand autonomous vehicles into broader fields of robotics.

The second is cost-effectiveness. US restrictions on advanced chips have spurred Chinese model companies to do more with less. This matters because the compute intensity of the Agent Era will be far higher than the Dialogue Era. For wide agent adoption, costs must fall dramatically. One holding, MiniMax, has developed open-source models approaching frontier capabilities at a fraction of the training cost, which is part of the wider Chinese ecosystem driving intelligence down the cost curve. Winning does not require low-cost models to triumph in every benchmark. They can win by making intelligence cheap enough to be embedded in software agents, consumer apps, enterprise workflows, robotics, and vehicles.

China's third advantage is demonstrated in our holding Bytedance: productization. ByteDance’s Doubao app shows how quickly generative artificial intelligence can become a consumer habit when deployed by a company that understands recommendation, interface design, and virality. Leading the Chinese market with over 226 million monthly active users. The next stage of AI will be shaped not just by those with the largest models, but also by those who can make intelligence cheap, useful, practical, and habitual.

Physical Supply Chain

The changes discussed above all directly impact the physical supply chain. Each era of generative artificial intelligence has heightened computing demand without eliminating previous demand. Model training was the initial driver in the era of Dialogue and that’s still expanding as frontier labs build ever larger models. The era of Reasoning added a second layer: models no longer just give answers, they spend more compute evaluating, checking logic, and considering alternatives before solving problems. The Agent Era introduces a third, fastest-growing layer of compute demand. Anthropic’s data show a single agent’s compute load is four times chat dialogue’s, and multi-agent systems consume about 15 times as much.

More significantly, so far the demand for AI has been implicitly limited by human attention. One person can only ask so many questions per day, and each answer must wait for the next prompt. Agents have effectively removed this constraint. Given a goal, an agent can iterate through reasoning dozens of times, operating autonomously while humans sleep, and increasingly collaborate with other agents on the same task.

The three eras add up to a compound computing S-curve, with none leveling off—each one steeper than the last. The result: chip demand continues to accelerate dramatically. This logic underpins our investments across the chip supply chain, including our largest holding TSMC and ASML, as well as Nvidia, in which we’ve steadily added to our position.

Investing in the supply chain is a bet on the growth of artificial intelligence itself, not on which company will ultimately capture it. No matter which application succeeds or which frontier model prevails, the underlying compute demand is fulfilled by a handful of firms. That’s why investing in the supply chain is an unusually attractive way to share in AI’s growth.

Revolutionary Patterns: We are keenly aware that the history of revolutionary technologies is also the history of market overshoots. Even the most transformative innovations, human and market psychology has a reliable capacity to misprice their trajectory.

In the 19th century, railway companies reshaped the modern economy. At their peak in the 1880s, they accounted for about 60% of the U.S. stock market, only for a series of downturns to wipe out vast amounts of capital. The canal boom of the late 18th century, and the fiber optic build-out of the late 1990s, followed the same pattern: real technological progress, real economic impact—and genuine financial excesses as well.

We should expect artificial intelligence’s development to echo that history. The rational response is not to shun technological revolution. It’s not a safe bet. If AI disrupts most industries, avoiding it does not eliminate risk—it only transfers risk. You may still end up holding businesses facing disruption rather than owning platform companies with generational advantages.

The harder task for investors is to stay invested, but focused: distinguishing enduring value from temporary exuberance, robust infrastructure from fragile applications, and companies merely invoking AI from those capable of converting it to durable economic advantage. The emergence of capable agents makes us even more convinced that demand for AI can keep expanding.

But history teaches humility. Revolution brings waste, disappointment, and overbuilding along the way. Our job is not to believe every claim about AI, but to own outstanding companies that stand to benefit as intelligence gets cheaper, stronger, and more broadly deployed.

Lawrence Burns

SMT Fund Manager

Baillie Gifford (Baillie Gifford)

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Ripple’s CEO Explains Why XRP Exists In Under 2 Minutes

Shibarium daily transactions fall 75% after brief spike in July

Ethereum forms golden cross against Bitcoin after June rally