The decentralized finance (DeFi) landscape is facing a stark reality check. While the industry often touts a vast ecosystem of innovation, a closer look at the balance sheets suggests that the space is becoming increasingly concentrated at the top.

According to the data of DefiLlama, the vast majority of the sector is struggling to find a sustainable pulse. Out of approximately 1,300 listed projects, a staggering 97.6% are failing to generate significant revenue. The rest hover near zero or, in some cases, post negative cash flow.

Extreme Concentration at the Top

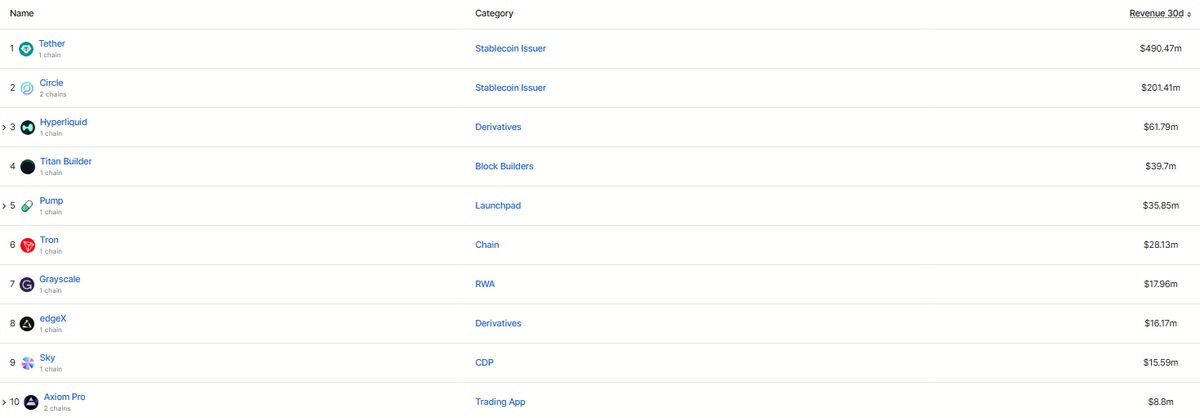

Revenue distribution follows a steep power-law pattern. Stablecoin issuers and high-velocity trading platforms dominate the top of the leaderboard, generating more than $50 million each: Tether at $490 million, Circle at $201 million, and Hyperliquid at $61 million.

Sponsored

Six protocols fell in the $10 million to $50 million range: Titan Builder ($39 million), which made headlines earlier this month by earning $34.5 million due to a user error, briefly surpassing giants like Tether, Pumpfun ($35 million), Tron ($28 million), Grayscale ($18 million), EdgeX ($16 million), and Sky ($15 million).

Source: DeFiLlama

Source: DeFiLlama

Most Projects Struggle for Profitability

Below the top tier, revenue drops off sharply. Ten protocols generated between $5 million and $10 million: Jupiter ($9.9 million), Axiom ($9.6 million), Ant Fun ($8.9 million), Phantom ($8.3 million), Fragment ($6.9 million), GMGN ($6.9 million), Aerodrome ($6.5 million), Aave ($6.4 million), Courtyard ($6 million), and Chainlink ($5.6 million).

Thirteen protocols recorded revenue between $2 million and $5 million: Fourmeme ($4.8 million), Polymarket ($4.4 million), Lido ($4.2 million), Lighter ($3.8 million), Base ($3.7 million), Pancakeswap ($3.6 million), Polygon ($3.4 million), Etherfi ($3.3 million), Collector Crypt ($3.1 million), Metamask ($2.9 million), Tradexyz ($2.8 million), Fomo ($2.6 million), and ORE ($2.2 million.

The numbers paint a picture of a “winner-take-most” market. Only 32 projects, a mere 2.4% of the total field, managed to cross the $2 million revenue threshold over the last 30 days.

The biggest losses over the past month were recorded by the MEV protocol Kairos Timeboost, which lost about $200,000, and the options platform Hegic, which reported a deficit of roughly $23,000.

Why This Matters

DeFi revenue remains heavily concentrated among a small group of dominant players, while most projects generate little to no meaningful income. The trend highlights growing fatigue with underused platforms that raised significant funding but failed to attract sustained user activity, widening the gap between top earners and the rest of the market.

People Also Ask:

Projects earn from transaction fees, lending interest, token emissions, or other on-chain activities. Revenue depends on user adoption and trading volume.

A few large protocols, like stablecoins and high-volume trading platforms, attract most users and fees.

By reviewing metrics like Total Value Locked (TVL), revenue generation, user activity, and token utility before investing.