Gap sees stronger sales at regular prices: Will average unit revenue keep rising?

Gap, Inc.: Strengthening Profitability Through Full-Price Sales

Gap, Inc. has been making significant progress in boosting its pricing strategy, with a clear move toward selling more items at full price. This shift has played a key role in enhancing the company’s profitability. As Gap continues to revitalize its brands, better product reception and improved merchandising have lessened the need for deep discounts. This change points to growing consumer trust in Gap’s offerings and indicates that the company’s recovery is increasingly driven by genuine demand rather than promotional sales.

Higher rates of full-price sales have led to an increase in average unit retail (AUR) across Gap’s main brands, supporting overall profit margins. In the fourth quarter of fiscal 2025, Gap reported a gross margin of 38.9%, a decrease of 80 basis points compared to the previous year, mainly due to a 200-basis-point impact from tariffs. However, underlying merchandise margins improved thanks to stronger full-price sales and fewer markdowns. The rise in AUR has helped cushion some of the cost challenges, especially in key categories like denim, fleece, and activewear, where customer interest remained high.

Operational improvements have also contributed to these gains. By tightening inventory controls and refining demand forecasts, Gap has been able to better match supply with customer needs, reducing excess stock and limiting the need for heavy promotions. Enhanced brand storytelling and marketing that resonates with current culture have further strengthened Gap’s image, allowing the company to hold firm on pricing without losing shoppers. These strategies underscore the importance of precise merchandising in driving both sales quality and profitability.

Looking ahead, Gap’s ability to maintain its AUR growth will depend on keeping its products relevant while managing external challenges such as tariffs, competitive pricing, and changing consumer preferences. If the apparel industry sees a rise in promotional activity, Gap may face renewed pressure to discount. However, ongoing innovation, leadership in key categories, and disciplined inventory management could help the company sustain its momentum in full-price sales, making AUR a key metric to monitor in the upcoming quarters.

Gap’s Stock Performance, Valuation, and Outlook

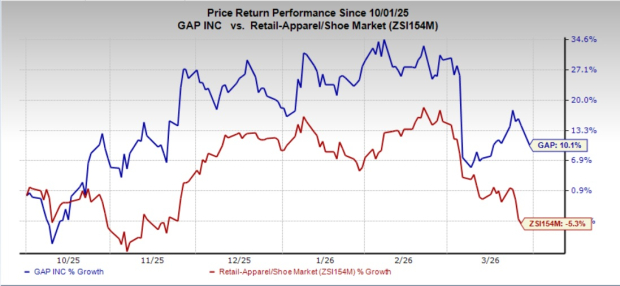

Over the past six months, Gap’s stock has risen by 10.1%, outperforming the retail apparel and shoes industry, which saw a decline of 5.3% during the same period.

Image Source: Zacks Investment Research

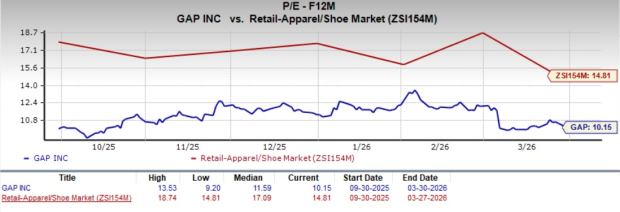

From a valuation perspective, Gap is currently trading at a forward price-to-earnings ratio of 10.15, which is lower than the industry average of 14.81.

Image Source: Zacks Investment Research

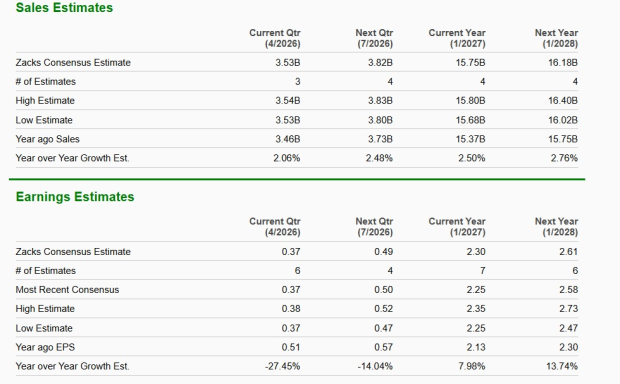

Consensus estimates from Zacks suggest that Gap’s sales and earnings for fiscal 2026 are expected to grow by 2.5% and 7.9%, respectively. For fiscal 2027, analysts anticipate a 2.7% increase in sales and a 13.7% rise in earnings.

Image Source: Zacks Investment Research

Other Noteworthy Retail Stocks

In addition to Gap, several other retail stocks have earned higher rankings and are worth considering:

- Deckers Outdoor Corporation (DECK): A leader in designing and managing innovative footwear and accessories, Deckers currently holds a Zacks Rank #1 (Strong Buy). The company’s consensus estimates project earnings and sales growth of 8.5% and 8.9%, respectively, for the current fiscal year. Deckers has also delivered an average earnings surprise of 36.9% over the past four quarters.

- Tapestry, Inc. (TPR): Formerly known as Coach, Tapestry designs and markets premium accessories and gifts for both men and women globally. The company also holds a Zacks Rank #1. Current estimates suggest earnings growth of 26.5% and sales growth of 11.2% for the fiscal year, with an average earnings surprise of 12.8% over the last four quarters.

- FIGS Inc. (FIGS): Specializing in direct-to-consumer healthcare apparel and lifestyle products, FIGS is ranked #2 (Buy) by Zacks. The company has posted an average earnings surprise of 187.5% over the past four quarters, and sales for the current year are expected to grow by 11.7% compared to last year.

Zacks’ Top Stock Picks

Zacks’ research team has identified five stocks with the potential to double in value in the coming months. Among these, the Director of Research, Sheraz Mian, highlights a lesser-known satellite communications company poised for significant growth as the space industry expands toward a trillion-dollar market. Analysts are forecasting a substantial revenue surge for this company in 2025. While not every top pick achieves outsized gains, this one could outperform previous winners such as Hims & Hers Health, which soared by over 200%.

Additional Resources

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

NextNRG’s $0.55 Debt-to-Equity Exchange Reflects Urgent Fundraising and Increased Dilution Threat

AQR Anticipates Quetta’s Recovery While Mizuho Silently Leaves the Delisting Dilemma

Pirelli Faces Critical Juncture: Board Resists Imposed Cyber Tyre Separation as Geopolitical Deadline Approaches